Tomas spent two decades building a career in Europe’s auto supply chain. Senior manager at an Italian multinational. A man who knew the industry from the inside, its rhythms, its margins, its plans. Then, in the autumn of 2025, he walked away from all of it.

“I think it’s doomed,” he told reporters. “The industry is doomed.”

He’s Czech. He asked that his surname not be used. And he’s not being dramatic, he’s being precise. Because what he watched unfold over his final years in that business is the same thing keeping executives awake in Frankfurt, Munich, and Stuttgart right now.

A Chinese EV revolution is coming for European carmakers. And it’s not coming slowly.

They Said It Couldn’t Happen Here

The old playbook said this was impossible. Chinese cars were cheap because they cut corners. European brand loyalty ran deep. Quality would always win. Customers would never trust a Chinese badge.

That playbook is no longer relevant.

In April 2025, BYD, “Build Your Dream,” still an odd name, an increasingly undeniable company, registered more battery-electric vehicles in Europe than Tesla for the very first time. The gap was close: 7,231 BYD registrations to Tesla’s 7,165, according to JATO Dynamics data covering 28 European nations. But the direction of travel? Not close at all. BYD’s sales were up 169% year-on-year. Tesla’s were down 49%.

One month, it’s a close race. Leave those trajectories running for twelve months, and you don’t have a race anymore.

The Numbers That Should Keep Stuttgart Up at Night

The April milestone was just the most visible moment in a much bigger story.

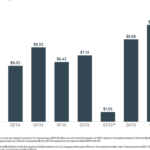

Chinese brands held barely 1% of Europe’s EV market at the start of this decade. By August 2025, that figure had reached 9.6%. In December 2025, BYD alone registered 27,678 vehicles across Europe, a 229.7% year-on-year surge, per ACEA data. Spain went from 3,801 BYD registrations in 2024 to 15,857 in 2025. Germany, the hardest market, the home turf of VW and BMW, went from 2,891 to 23,306. That’s a 706% jump in a single year.

And BYD isn’t the only name in this story. Xpeng is eyeing European expansion with its mass-market Mona series, which starts at the equivalent of roughly $17,000 in China. GAC is targeting 50,000 European sales by 2027. Nio has showrooms in Berlin. This isn’t a single brand making a push; it’s an industry arriving.

Now look at what’s happening to the Europeans in China. German carmakers held a 24% share of China’s car market in 2020. By 2024, that had collapsed to 15%. In Q3 2025, Mercedes-Benz China sales fell 27%, the sharpest quarterly drop since 2016, according to Bloomberg. Mercedes’s full-year 2025 operating profit fell 57%, with revenue down 9% to €132.2 billion. The company is now cutting up to 30,000 jobs and targeting €5 billion in savings by 2027.

That’s not a rough patch. That’s erosion.

BYD’s Secret Weapon Isn’t the Car – It’s the Price

Here’s what makes this different from previous waves of automotive competition: the Chinese advantage isn’t just labour costs. It’s a structural moat built over fifteen years that Europe can’t replicate quickly.

Start with pricing. The BYD Dolphin Surf, a proper, five-star Euro NCAP-rated city car, starts at €19,990 in Europe. The BYD Seal U plug-in hybrid lists from €39,990 in Germany, where it became Europe’s best-selling PHEV in 2025, outselling over 72,000 units. For comparison: the Volkswagen Tiguan eHybrid starts at €52,215. The Volvo XC60 PHEV begins at €67,990. That’s a gap of over €12,000 to €28,000 against established European brands, even after EU tariffs have been added to BYD’s sticker price.

How is this possible? Supply chain control at a scale European manufacturers simply don’t have.

China holds 85% of global battery cell production capacity. It refines over 90% of the world’s graphite, around 80% of cobalt, and approximately 60–70% of lithium, the core minerals in every EV battery on the road. The IEA’s 2025 Global Critical Minerals Outlook found that China is the leading refiner of 19 out of 20 key strategic minerals, with an average market share of 70% across them. And in 2025, 70% of all EVs produced globally came from China. (That’s not a typo.)

BYD doesn’t just assemble cars. It produces its own batteries, its own chips, its own steel. Every link in the chain sits inside the same company, or inside China’s state-supported industrial ecosystem. European carmakers, by contrast, are buying components from suppliers who are buying materials that originated in China. The inefficiency and the vulnerability compound at every stage.

Building Factories Inside the Walls

When the EU introduced tariffs on Chinese-made EVs in late 2024, an extra 17% for BYD on top of the standard 10% import duty, Brussels thought it had bought European industry some breathing room.

BYD’s answer was to start building inside Europe.

Its Szeged, Hungary plant, a €4 billion investment on a 300-hectare site, began trial production in Q1 2026. Mass production is scheduled to follow in Q2 2026. Phase one annual capacity is 150,000 vehicles, with expansion to 300,000 planned. A second facility in Manisa, Turkey, is also ramping up in 2026, and one source close to the project told Reuters that the Turkish plant is expected to out-produce Hungary as early as 2026, partly because labour costs there are substantially lower. A third European plant, reportedly in Spain, is under active consideration.

Cars built in Hungary and Turkey don’t carry the same additional tariffs as imports from Shenzhen. The wall Brussels built? BYD is manufacturing its way around it, legally, systematically, and faster than most analysts expected.

The retail footprint is expanding just as fast. BYD had approximately 1,000 points of sale across 29 European countries by the end of 2025, and is planning to double that number in 2026. The playbook is exactly what Toyota ran in the 1980s: get the cars near the customers, make service accessible, and build familiarity through proximity. It worked then. There’s no reason to think it won’t work now.

Europe Is Fighting Back. But Is It Fast Enough?

The legacy carmakers aren’t ignoring this. They’re not standing still.

BMW’s “superbrain architecture”, a centralised computer system replacing distributed hardware, was one of the marquee announcements at IAA Munich 2025. Volkswagen has teamed up with Xpeng to develop China-specific EV platforms, cutting local development costs by 40%. Mercedes is investing through joint ventures to produce models built exclusively for the Chinese market. These are real moves, not press releases.

And European brands still have something Chinese companies don’t: decades of trust. Surveys consistently show European buyers are hesitant to choose a brand they don’t recognise. Heritage matters. Engineering reputation matters. The Chinese brands know this, which is why they’re investing heavily in marketing, European celebrity partnerships, and dealer network expansion, precisely to close that perception gap.

But trust erodes when the price gap is €12,000 to €28,000. And Counterpoint Research’s analysts have noted the core tension clearly: “Europe’s automakers still hold significant brand value and legacy. The challenge lies in achieving production at scale and adopting new technologies faster.”

Brand value buys time. It doesn’t win wars.

Europe already surrendered its solar panel manufacturing to China, not because Chinese solar panels were better at first, but because they were cheaper, and cheaper. The auto executives who watched that happen are now running car companies. They know exactly what the precedent looks like.

The Clock Is Ticking

BYD is targeting 1.3 million overseas sales in 2026, a 24% increase on an already record-breaking year. It operates in 29 European country markets. Its cars are on the streets of Berlin, Oslo, Madrid, and London. Its factories are opening inside EU borders. Its dealer network is doubling.

The Chinese EV threat to European carmakers isn’t a warning on the horizon. It’s already in the showroom.

Tomas, the supply chain veteran who walked away from a two-decade career, wasn’t making a prediction when he said the industry was doomed. He was describing what he’d already seen from the inside, the cost structures, the technology gap, and the pace of change, and concluding that the traditional European automotive model didn’t have a convincing answer.

Maybe he’s wrong. Maybe BMW’s software bets pay off. Maybe VW’s China partnerships unlock the scale they need. Maybe tariffs buy enough time for European battery manufacturing to reach cost parity.

But the factories are opening. The prices are dropping. The cars are arriving.

What happens next is up to the Europeans to decide, and the window to decide is getting narrower every month.